according to the report. The outlook suggests beverage manufacturers consider smaller markets and accept that in North America and Western Europe soft drink sales will remain stagnant, providing an opportunity for water and ready-to-drink tea.

“Bottled water is the clear leader in global soft drinks volume growth, with over 242 billion liters which was 38% of total soft drinks volume in 2012,”according to the report. Growth of 5% per year is expected through 2017. Water will deliver 55% of projected volume growth in soft drinks.

Due to the negative health image of CSDs, volume of carbonated beverages will continue to slide and value is projected to decline 1% in North America through 2017 with less than 1% growth in China, according to Euromonitor.

“Both Coca-Cola and PepsiCo are struggling to find any growth in CSDs as consumers shift to healthier alternatives, such as bottle water and ready-to-drink (RTD) teas,” according to the report.

“Growth of soft drinks will continue to move to lower priced, emerging markets meaning volume growth will continue to exceed value growth,” according to the report.

according to the report. The outlook suggests beverage manufacturers consider smaller markets and accept that in North America and Western Europe soft drink sales will remain stagnant, providing an opportunity for water and ready-to-drink tea.

“Bottled water is the clear leader in global soft drinks volume growth, with over 242 billion liters which was 38% of total soft drinks volume in 2012,”according to the report. Growth of 5% per year is expected through 2017. Water will deliver 55% of projected volume growth in soft drinks.

Due to the negative health image of CSDs, volume of carbonated beverages will continue to slide and value is projected to decline 1% in North America through 2017 with less than 1% growth in China, according to Euromonitor.

“Both Coca-Cola and PepsiCo are struggling to find any growth in CSDs as consumers shift to healthier alternatives, such as bottle water and ready-to-drink (RTD) teas,” according to the report.

“Growth of soft drinks will continue to move to lower priced, emerging markets meaning volume growth will continue to exceed value growth,” according to the report.

Fruit juice volume is expected to grow by 3% in 2014. This growth is dominated by BRICs, which together account for almost 60% of the total increase in liters.

“The global tea marketplace remains highly fragmented and therefore provides ample room for large tea companies to expand across international markets in 2014. This is especially so for China, which is forecast to account for half of global tea growth through 2017, according to the report.

There has been limited merger-and-acquisition activity and industry consolidation in the tea segment has been slow, according to Rabobank analyst Ross Colbert. The top ten global tea brands account for 30% of the total tea market, estimated at $40.7 billion. Unilever (Lipton) holds an 11.7% share of retail value with Tata Global Beverages (Tetley) with a 3.1% share and American British Foods (Twinings) with a 2.5% share.

“These three are the only truly global competitors in tea, and while they remain strong in mature markets across western Europe and North America, their challenge is to continue growing organically and penetrate the important tea markets of China, Russia and Japan,” according to the report.

China, which is the world’s largest tea producer has a low per capita consumption outside the tea growing regions. The country is forecast to account for half of global tea growth through 2017. Unilever’s market share in China is 1.6% “and neither Tata nor Twinings have any presence there today.” These companies will have to acquire or establish partnerships with local players and develop new lines to meet the demand for products like Strong Milk Tea (black tea sweetened with condensed milk) and Xian Piao Piao (instant milk tea).

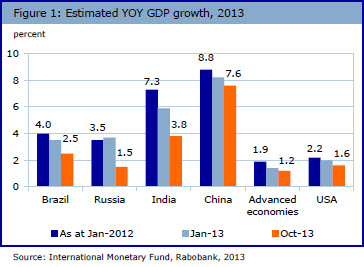

“Beverage companies must now adapt to slower growth in BRIC markets by implementing new strategies to reach consumers more efficiently,” writes Colbert.

“Strategic initiatives such as direct-to-consumer selling, co-manufacturing and developing more efficient distribution platforms can help mitigate the impact of softer volumes in BRIC markets,” he said. Learn more: Rabobank Food & Agribusiness

Source: Rabobank

Fruit juice volume is expected to grow by 3% in 2014. This growth is dominated by BRICs, which together account for almost 60% of the total increase in liters.

“The global tea marketplace remains highly fragmented and therefore provides ample room for large tea companies to expand across international markets in 2014. This is especially so for China, which is forecast to account for half of global tea growth through 2017, according to the report.

There has been limited merger-and-acquisition activity and industry consolidation in the tea segment has been slow, according to Rabobank analyst Ross Colbert. The top ten global tea brands account for 30% of the total tea market, estimated at $40.7 billion. Unilever (Lipton) holds an 11.7% share of retail value with Tata Global Beverages (Tetley) with a 3.1% share and American British Foods (Twinings) with a 2.5% share.

“These three are the only truly global competitors in tea, and while they remain strong in mature markets across western Europe and North America, their challenge is to continue growing organically and penetrate the important tea markets of China, Russia and Japan,” according to the report.

China, which is the world’s largest tea producer has a low per capita consumption outside the tea growing regions. The country is forecast to account for half of global tea growth through 2017. Unilever’s market share in China is 1.6% “and neither Tata nor Twinings have any presence there today.” These companies will have to acquire or establish partnerships with local players and develop new lines to meet the demand for products like Strong Milk Tea (black tea sweetened with condensed milk) and Xian Piao Piao (instant milk tea).

“Beverage companies must now adapt to slower growth in BRIC markets by implementing new strategies to reach consumers more efficiently,” writes Colbert.

“Strategic initiatives such as direct-to-consumer selling, co-manufacturing and developing more efficient distribution platforms can help mitigate the impact of softer volumes in BRIC markets,” he said. Learn more: Rabobank Food & Agribusiness

Source: Rabobank