In a typical year supply and demand fundamentals dictate market trends. Trading tea in 2018 was anything but typical and there are signs that significant disruptions will emerge in the New Year.Global trade expanded for a generation as nations lowered barriers to commerce. The trend slowed in 2018. This photo depicts a massive freighter approaching the greatly expanded locks at the Panama Canal.

Tariffs troubled global markets in 2018 but did not seriously impede trade in tea. However, sanctions restricting sales to Iran, the world’s fifth largest tea importer, and political unrest in Sri Lanka pose a greater threat in 2019.

Trade in agricultural commodities during the year was seriously disrupted as the U.S. attempted to curb Chinese trade practices. Several blows and counter-blows involving billions of Chinese goods left American farmers and small Chinese manufacturers the hardest hit.

A June skirmish in the trade war with the U.S. led China to increase import duties on American tea and coffee by 10 percent. In September, after the U.S. began taxing an additional $250 billion in Chinese goods, China again raised duties. Tariffs now total 35 percent on tea imported from the U.S. but the impact is negligible. China, the world’s largest tea producer, imports only 2 percent of the world’s tea, spending $149.4 million in 2017. Few U.S. based companies sell tea to the Chinese.

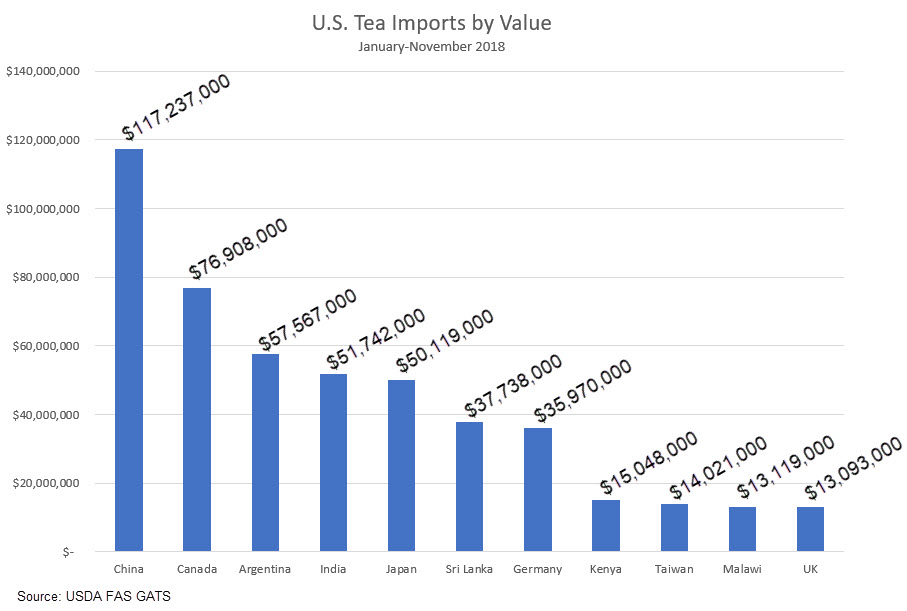

During the period June through October Chinese tea imports for consumption in the U.S. totaled $117 million, up 10 percent compared to the same period in 2017 on a volume increase of 6 percent, according to USDA Foreign Agricultural Service (FAS) statistics. Green tea imports from China, at 4.7 million kilos, showed the biggest gains – up 20 percent in value and 24 percent in volume. These totals suggest some stockpiling in anticipation of rising duties.

During the G20 Summit in Argentina in late November the U.S. renewed its threat to retaliate across the entire spectrum of Chinese imports, effective January 1. That would have imposed at least a 10 percent duty on Chinese tea imports, but President Donald Trump called a truce in early December and the two countries resumed negotiations for 90 days. Markets remain unsettled as the price of stocks experienced a steep decline. The deal under consideration calls for significant purchases by the Chinese to help balance a persistent trade deficit.

China ranked third in volume, behind Canada and Argentina, as a supplier of tea for U.S. consumers, according to FAS. The country retains its position as the most valuable U.S. tea trade partner, first overtaking Canada in 2010 and continuing to widen the gap.

During the first 10 months of the year China shipped 17.8 million kilos of tea to the U.S., less than half the 41.4 million arriving from Argentina, but importers paid an average $6.57 per kilo for Chinese imports compared to $1.39 per kilo for Argentine tea, most of which is used to make iced tea and instant.

The U.S. trade war with China, Europe, and with neighboring North American countries caused a lot of collateral damage in commodities but taxing tea is not a big concern.

Margins would suffer should negotiations with China fail but American retailers believe consumers will accept a 10 percent (65-cent per kilo, 30-cent per pound) increase. The current NTR (normal trade relations) duty on green tea, packaged 3 kilos and smaller, is 6.4 percent, effective April 26, 2018. Should negotiations fail, and the U.S. were to match the putative 35 percent duties now enforced by China, the price for consumers would rise by $2.25 to almost $9 per kilo on average, a threshold that would surely lead importers to source green tea from Indonesia, Vietnam, Thailand, and Taiwan ― anywhere but China.

Emerging Threats to TradeSanctions that limit Iran’s ability to trade in U.S. dollars are now in full force. Iran produces only a small fraction of the 120 million kilos of tea it consumes annually, spending about $283.8 million in 2017 to import several million kilos. Since tea is traded in dollars, sanctions significantly impact tea imports from India, Sri Lanka, and Kenya. Once sanctions, first imposed in 2012, were lifted the economy surged and Iran went on a tea spending spree. The new round of sanctions likely means a return to austerity.

The latest sanctions include a U.S. threat of financial restrictions on countries that continue to trade with Tehran. In 2012 India and Sri Lanka “exchanged” oil for tea. That is less likely during this round as Sri Lanka owes Iran $250 million for oil. A spokesman for the Iran tea organization Goudarz Khordadpour, said that tea imports would not exceed 55,000 metric tons, worth approximately $275,000. Tea is not banned, and the U.S. is unlikely to go so far as a blockade, but the U.S. intends to prevent financial circumventions from occurring. The average price of orthodox tea fell to $2.81 in 2018, down from $3.08 per kilo in 2017, largely because of the decline in shipments to Iran. Since Iran buys most of its tea from India, sanctions may force India to export its tea elsewhere.

Developments in Sri Lanka are more troubling. The tea auction in Colombo, the world’s largest, remains above the fray, but a constitutional crisis to determine who will govern raises the possibility of civil unrest. Sri Lanka is now the world’s second largest tea exporter by value, accounting for 19.3 percent of global tea and earning $1.5 billion in 2017.

Tea production accounts for 2 percent of the national economy, employs millions and was at the heart of a 25-year civil war ending in 2009. The war resulted in $200 billion of economic damage, virtually eliminated foreign investment and curtailed auction activities, shifting trade to India and Kenya.

An extended drought reduced production totals in 2018 and a December strike by 100,000 Sri Lanka plantation workers continues indefinitely. Workers began daily protests in October seeking to double their daily wage. The Planters Association of Ceylon (PA) said the strike is costing plantation companies $1.4 million a day.

The PA propose a revenue sharing alternative in which farmers would receive 1,000 or more tea bushes to tend, receiving all proceeds after plantation companies deduct expenses and profits.

The Ceylon Workers Congress (CWC) is pressing for a $225 monthly salary for tea workers. CWC is the nation’s largest union of plantation workers but there is no solidarity in labor due to the fact unions are on opposite sides of the ongoing political battle. Leaders of the National Union of Workers (NUW), the Democratic People’s Front (DPF) and the Up-Country People’s Front (UPF) told their members not to strike.

Global Trade

Global shipments for 2018 are still being tallied but are on par with 2017 totals, continuing a downward trend in value due to bountiful supply. Many countries continue to expand their production capability without paying heed to the fact that there is an estimated surplus of 75,000 metric tons in 2018 that is expected to rise to 128,000 metric tons in 2020, according to The Economist Intelligence Unit (EIU) citing United Nations FAO estimates.

As a result, prices are expected to continue to decline to a global average of $2.79 per kilo, down from $3.19 per kilo in the third quarter of 2017. Global tea imports for all tea buying nations were estimated at $7.349 billion in 2017.

Asia continues to drink most of the world’s tea, consuming most of what it produces and exporting 60.3 percent of the global total, worth $4.7 billion.

China is among the five fastest growing tea exporters, growing 29.3 percent by value since 2013.

The U.S. and Germany remain China’s most valued import markets. The U.S. spent $486.8 million importing 6.7 percent of the word’s tea in 2017 while Germany spent $255.2 million importing 3.1 percent of the world’s tea.

During the first 10 months of 2018 the U.S. spent $117 million on Chinese tea, a 10 percent increase over the same period in 2017.

Exports declined 2.4 percent in 2018 according to the Sri Lanka Tea Exporters’ Association (TEA) which reported 235.6 million kilos shipped during the period January through October. Production is down overall. Sri Lanka’s biggest trading partner is Iraq followed by Turkey, Russia, and Iran. Sales to Iran are likely to be impacted due to sanctions.

Sri Lanka consistently produces high-quality teas that brings top prices at auction. India, by comparison, earned only $591.2 million in 2017. India exports were valued at $560 million through October, up from $537 during the same period last year. Volume was 200 million kilos making India the 4th largest tea exporter ahead of the United Arab Emirates. UAE grows no tea, but it is the world’s most important re-exporter of tea, accounting for 3.7 percent of the global total.

Africa is the next most productive origin, accounting for 13.2 percent of worldwide tea shipments. The weather was good and tea exports from East Africa were strong in 2018, up 13 percent across the region. Prices however are soft. Kenya, the largest of Africa’s growers, will export 7.6 million kilos in 2018, up 11.4 percent compared to 2017. In 2017 Kenya earned $1.4 billion from exports.

Unfortunately Kenya's good production totals led to a two-year low at the Mombasa auction where average prices fell to $2.12 per kilo in December. During the same period in 2017 auction prices averaged $2.59 per kilo.

Latin America exports 2.3 percent of the world’s tea and Oceania, including Australia, ships 0.2 percent.

Tea sales in the European markets are flat, due in part to lingering economic doldrums and the ongoing realignment of the European Union. EU consumes 4 percent of the world’s tea and expected to grow by 1.2 percent.

Russia remains the biggest tea importer, consuming 2.5 percent of the world’s tea. Ramaz Chanturiya, chair of the Tea Association of Russia, said the country imported more than 170,000 metric tons in 2018. India, which supplies about 30 percent of Russian imports, is pressing for a reduction in duties on packet tea (currently 12.5 percent). Russia was India’s most important trade partner by value until recently when Iran, freed temporarily of U.S. sanctions, bought more tea. Russia remains India’s biggest tea trade partner by volume. India hopes to increase its exports to Russia to 65 million kilos in 2020 from 48 million in 2018.

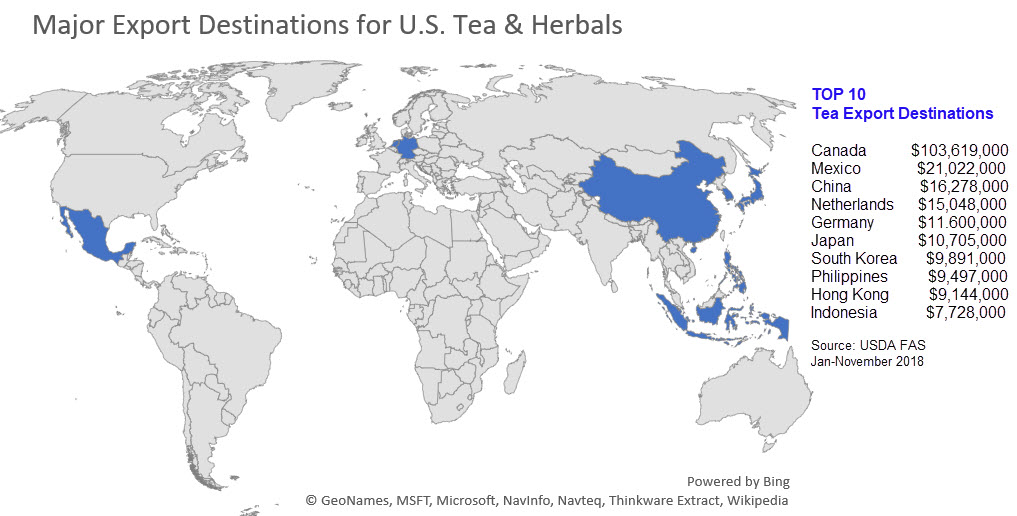

U.S. Tea Exports US Tea Exports Jan-Nov 2018U.S. Tea Exports

The United States is a major consuming market and while it produces very little tea, it ranked 9th among the world’s tea exporting countries at $136.1 million (ahead of Japan and just behind the United Kingdom).

It is among the five fastest growing tea exporters, growing 39.9 percent by value since 2013.

During the first 10 months of 2018 shipments were up 5 percent overall on $316 million in revenue.

The country’s most important trade partner is Canada, which imported 19.5 million kilos in 2017, spending $124 million. Tea exports to Canada are up 3 percent in the first 10 months of 2018 but value flat at $104 million during the first 10 months of the year. Canadians will buy about $125 million of U.S. tea in 2018.

The Germans also buy a lot of U.S. processed tea. In 2017 the German market was second to Canada in volume and value. A five-year trend is evident, in 2013 Germany purchased 1.6 million kilos for $8 million. In 2017 they paid $12 million for 1.9 million kilos. Imports for the first 10 months of 2018 were 2.4 million kilos, valued at $11.6 million, a 34 percent increase in quantity and 18 percent increase in value (paying an average $4.95 per kilo). Similarly, The Netherlands also spent 18 percent more on tea than in 2017 for 52 percent increase in volume (paying an average $8.14 per kilo).

As an aside, China bought an unusually large quantity of U.S. tea in 2018, likely anticipating a steep increase in duties but also reflecting a strong interest in black teas by China’s younger tea drinkers. Singapore also imported a large quantity of U.S. made tea.

Market Fundamentals

A review of market fundamentals suggests three powerful trends continue to drive sales ― oversupply; growing affluence driving an up-market move to premiumization and worldwide awareness that tea is a healthy beverage. Consumption is rising at surprising rates in developing countries where tea is grown. China now consumes 40 percent of the world’s tea and dominates the green tea category. Still, China only exports 15 percent of its tea. India is similarly positioned. China and India together now drink 59 percent of the world’s tea, up from 40 percent in 2010. Domestic consumption in India grew by 6 percent in 2018. During the period 2019-20 EIU forecasts the tea industry globally will grow by 4.6 percent.

Tea ready for shipment (Photo/Dan Bolton)

Countries losing market share by value including Vietnam, Indonesia, the UK and Argentina. Vietnam is the fifth largest tea exporting country and very much aware of the decline. Sales average $1.60 per kilo. The country has 125,000 hectares under tea, mainly in the northern mountainous provinces of Thai Nguyen, Ha Giang, Phu Thọ, Tuyen Quang and Yen Bai, and the Central Highlands province of Lam Dong. Dr Nguyen Huu Tai, Chairman of the Vietnam Tea Association, expects exports to total 145,000 metric tons in 2018, earning $245 million. Vietnam grows much more green tea than in the past. It now accounts for 55 percent of total production. Domestic consumption is also growing, Vietnamese drank 45,000 metric tons of tea in 2018.

Sales of green tea in the black tea producing countries of Africa and India is an example of how the world’s tea drinkers are expanding their preferences to include diverse teas of the world. One of the most significant trends in trade is the growing popularity of black tea in Asia where young people are driving sales.

“Global demand for black tea will continue to rise, driven in particular by its increasing popularity in China, but the pace of growth will be outstripped by that for green tea, fruit tea, herbal tea, rooibos (from South Africa), purple tea (mainly from Kenya) and high-end organic tea, reflecting their greater reported health benefits and heavy marketing,” according to EIU.

Sources: Economist Intelligence Unit, United Nations FAO

Market Fundamentals

A review of market fundamentals suggests three powerful trends continue to drive sales ― oversupply; growing affluence driving an up-market move to premiumization and worldwide awareness that tea is a healthy beverage. Consumption is rising at surprising rates in developing countries where tea is grown. China now consumes 40 percent of the world’s tea and dominates the green tea category. Still, China only exports 15 percent of its tea. India is similarly positioned. China and India together now drink 59 percent of the world’s tea, up from 40 percent in 2010. Domestic consumption in India grew by 6 percent in 2018. During the period 2019-20 EIU forecasts the tea industry globally will grow by 4.6 percent.

Market Fundamentals

A review of market fundamentals suggests three powerful trends continue to drive sales ― oversupply; growing affluence driving an up-market move to premiumization and worldwide awareness that tea is a healthy beverage. Consumption is rising at surprising rates in developing countries where tea is grown. China now consumes 40 percent of the world’s tea and dominates the green tea category. Still, China only exports 15 percent of its tea. India is similarly positioned. China and India together now drink 59 percent of the world’s tea, up from 40 percent in 2010. Domestic consumption in India grew by 6 percent in 2018. During the period 2019-20 EIU forecasts the tea industry globally will grow by 4.6 percent.

Market Fundamentals

A review of market fundamentals suggests three powerful trends continue to drive sales ― oversupply; growing affluence driving an up-market move to premiumization and worldwide awareness that tea is a healthy beverage. Consumption is rising at surprising rates in developing countries where tea is grown. China now consumes 40 percent of the world’s tea and dominates the green tea category. Still, China only exports 15 percent of its tea. India is similarly positioned. China and India together now drink 59 percent of the world’s tea, up from 40 percent in 2010. Domestic consumption in India grew by 6 percent in 2018. During the period 2019-20 EIU forecasts the tea industry globally will grow by 4.6 percent.

Market Fundamentals

A review of market fundamentals suggests three powerful trends continue to drive sales ― oversupply; growing affluence driving an up-market move to premiumization and worldwide awareness that tea is a healthy beverage. Consumption is rising at surprising rates in developing countries where tea is grown. China now consumes 40 percent of the world’s tea and dominates the green tea category. Still, China only exports 15 percent of its tea. India is similarly positioned. China and India together now drink 59 percent of the world’s tea, up from 40 percent in 2010. Domestic consumption in India grew by 6 percent in 2018. During the period 2019-20 EIU forecasts the tea industry globally will grow by 4.6 percent.